How Your Home Can Pay You Back at Tax Time

April 10, 2025

Homeowner Tax Benefits

April 10, 2025

Homeowner Tax Benefits

Most people think of homeownership as one big expense. And I get it, between mortgage payments, maintenance, insurance, taxes… the list seems never-ending. But what often gets overlooked is the way your home can pay you back when tax season rolls around.

If you're a homeowner, you may be sitting on deductions and credits that could reduce your taxable income, boost your refund, or soften the blow of what you owe. Here's how to take full advantage of that financial upside.

Let’s break down the most common tax perks homeowners may qualify for:

You can deduct interest paid on your mortgage for up to $750,000 of debt ($375,000 if married filing separately). This can be a major write-off in the early years of your mortgage when interest makes up most of your monthly payment.

You can deduct up to $10,000 in combined state and local property taxes (or $5,000 if filing separately). Just make sure you're itemizing your deductions to claim it.

If you’re self-employed and use part of your home exclusively for business, you may be able to deduct a portion of your home expenses—like utilities, rent or mortgage interest, and internet.

Made any upgrades like new insulation, windows, or solar panels? The IRS offers credits of up to 30% of the cost for qualifying improvements.

So how does owning a home really stack up when tax season hits? Here's a quick breakdown of how renters and homeowners compare when it comes to tax benefits.

Renters:

Pay monthly rent with no long-term return

Can’t deduct property taxes

Limited or no tax benefit for a home office

Any upgrades or improvements benefit the landlord

No equity building or tax-based advantages

Homeowners:

Mortgage payments may offer a mortgage interest deduction

Can deduct up to $10,000 in state and local property taxes

Home office deduction available for self-employed individuals

May qualify for energy efficiency tax credits (up to 30%)

Build equity over time plus tax advantages

Before you file, here’s what to gather and review:

Form 1098 – From your lender; shows how much mortgage interest you paid

Property tax statements – Track what you paid through the year

Receipts for home improvements – Especially energy-efficient upgrades

Home office documentation – Square footage, utility bills, and business use records

Closing documents – If you bought or sold a home in the past year

Records of energy credits claimed – For multi-year upgrades (like solar)

Owning a home can absolutely pay you back if you know where to look. And while this gives you a solid head start, your situation may involve additional savings opportunities.

Talk to a tax pro before you file, especially if you sold your home, worked from home, or made major upgrades last year.

Stay up to date on the latest real estate trends.

July 10, 2025

ow to Maximize Your Sale Price: 5 Mistakes to Skip When Selling

July 3, 2025

The 30% Rule is Dead. Here’s the New Way to Budget for a Home

June 26, 2025

5 Reasons Homebuyers Are Finally Catching a Break

June 19, 2025

The Biggest Real Estate Forecasts for the Second Half of 2025

June 12, 2025

Home Equity Is Surging. Borrowing Just Got Cheaper. Should You Tap In Now or Wait?

June 5, 2025

Warren Buffett Analysts Call This Trend a Housing Goldmine

May 29, 2025

Home Projects with the Highest ROI (and Joy) in 2025

May 22, 2025

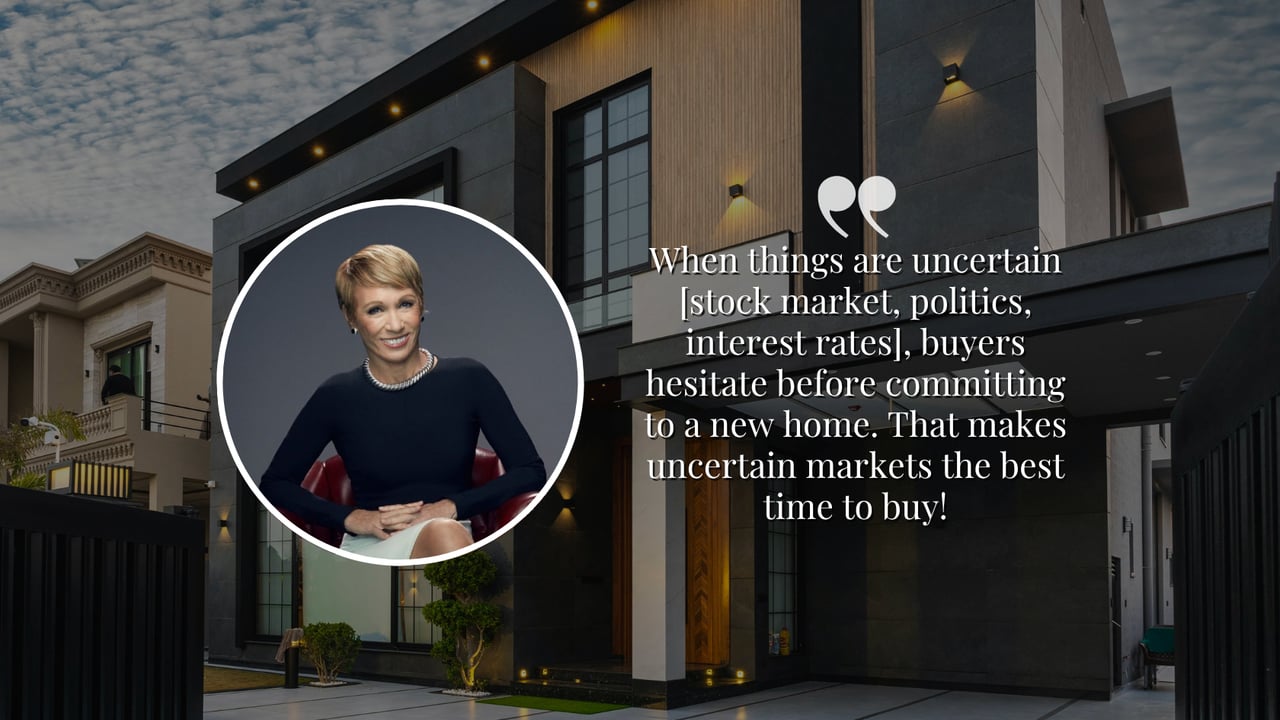

Barbara Corcoran’s 3 Tell-Tale Signs That It’s a Good Time to Buy a Home

May 15, 2025

The 3 Rooms that Can Make or Break a Sale

You've got questions and we can't wait to answer them.